The Rise and Fall of American Growth: A summary

by Jason Crawford · October 5, 2020 · 12 min read

The Rise and Fall of American Growth, by Robert J. Gordon, is like a murder mystery in which the murderer is never caught. Indeed there is no investigation, and perhaps no detective.

The thesis of Gordon’s book is that high rates of economic growth in America were a one-time event between roughly 1870–1970, which he calls the “special century”. Since then, growth has slowed, and we have no reason to expect it to return anytime soon, if ever.

The argument of the book can be summarized as follows:

- Life and work in the US were utterly transformed for the better between 1870 and 1940, across the board, with improvements continuing at a slower pace until 1970.

- Since 1970, information and communication technology has been similarly transformed, but other areas of life (such as housing, food, and transportation) have not been.

- We can see these differences reflected in economic metrics, which grew significantly faster especially during 1920–70 than before or since.

- All of the trends that led to high growth in that period are played out already, and there are none on the horizon to replace them.

- Therefore, high growth is a thing of the past, and low growth will be the norm for the future.

The bulk of the book’s 700+ pages are dedicated to the first three points above: a qualitative and quantitative survey of how the American standard of living has changed since 1870.

In the several decades after 1870, every aspect of American life was transformed:

-

Food: In 1870 Americans were well-fed, but with a monotonous diet high in pork and cornmeal, foods that could easily be preserved without refrigerators. Over the coming decades diets became more varied, and food got easier to prepare, thanks to the introduction of home refrigerators, prepared foods, and supermarkets. But major innovation here was over by 1940.

-

Clothing: In 1870 most Americans owned only a few outfits. Most clothing was made in the home, by women, although some men’s clothing might be purchased. By 1940 clothing was made in factories and purchased through department stores and other retail outlets.

-

Retail: The general store of 1870 gradually gave way to the urban department store, with better selection and lower prices, and rural areas were served by mail order catalogs, which took advantage of the postal service and the railways. Later, when cars became common, people had more shopping options because they could drive to the city, ending the monopoly of local stores in small towns.

-

The home: Many big changes occurred 1870–1940. Homes got electricity, running water, sewage, gas, and telephone service; Gordon summarizes this as the home becoming “networked.” No more did people have to haul water from the well, or carry wood and coal into the house to be burned in the kitchen stove, and then to carry the dirty water and burnt ashes outside again. Homes got bathrooms with toilets to replace outhouses, and private bathtubs to replace the previous more public practice of bathing in the kitchen, with water heated on the stove. (Hauling and heating the water was laborious enough that most people bathed no more than weekly.) Central heating meant that bedrooms received heat, instead of just the kitchen. Electricity, and the advent of labor-saving appliances such as the washing machine, simultaneously improved cleanliness and reduced total housework. And gas light was replaced by clean, safe, convenient electricity.

-

Transportation: Although railroads were fairly well established by 1870 (with the first transcontinental railroad having been completed in 1869), this only solved the problem of transit between major cities. Within cities, and on the last mile between the railroad and destinations such as individual farms, people still depended on horses. Horses were expensive to care and feed (a lot of US agriculture was devoted just to this purpose), they littered the streets with their urine and manure, and they could pull a load at only a few miles per hour. We escaped the “tyranny of the horse” starting with electric streetcars in the early 1900s, and then completely with the internal combustion engine and the automobile, which became affordable with the Model T turned out by Ford’s assembly line in the 1910s. By 1940 the automobile had fairly taken over American life. The major developments in transportation after this were the interstate highway system and commercial air travel, both of which were well established by 1970.

-

Communications: In 1870, communications were by postal mail, or by (expensive) telegram. Rural families in particular were extremely isolated. The years 1870 to 1940 saw the development of the telephone, phonograph, movies, and radio. By 1940, then, people could talk to family, friends, and business associates anywhere in the country (or even across the ocean, if it was worth the high price); they could listen to recorded music from great performers, and go to the cinema to see shows and (in the early days) newsreels; and they could tune in to real-time news, entertainment, and sports broadcasts. Between 1940 and 1970, the television industry grew, and television replaced some of the functions of film and radio.

-

Health & disease: In 1870 the germ theory was still being established, and it had yet to make any impact on American life. But in the coming decades, water filtration and chlorination was established in all major cities, milk became pasteurized, and the Food & Drug Administration (created 1906) began enforcing standards of purity and safe handling on meat, milk, and medicines. Mortality rates dropped quickly. And then between 1940 and 1970, antibiotics were discovered to treat most bacterial diseases.

-

Work: Work life improved for both men and women. For men, work shifted from dangerous and uncomfortable manual labor on farms to safer and more comfortable jobs indoors. Some of that work was routine, but an increasing share of it is not. For women, the great liberation was the reduction in the need for housework, thanks to the changes mentioned above: running water, electric appliances, and products such as premade clothes and prepared foods. This led to a big increase in women in the workforce after World War II.

However, many of these areas of life have seen comparatively minor improvements since 1970 and some of them since 1940:

-

Food and clothing have seen only minor changes since 1940, with some new products and new types of stores.

-

The home has seen modest improvements. Home sizes have steadily increased. The quality of appliances, including their reliability, improved steadily mid-century but was mostly complete by 1970 (based on an extensive survey of Consumer Reports magazine). The biggest changes since 1970 have been the microwave oven and the spread of air conditioning.

-

Transportation is fundamentally unchanged since the 1970s, after jet engines became common in air travel. Indeed, air travel has regressed on some dimensions, such as tighter seating and longer security lines.

-

Medicine has not had a revolution since 1970 comparable to the germ revolution, and the main treatments for cardiovascular disease and cancer already existed in 1970, although there have been some notable improvements such as the reduction in lung cancer from smoking.

-

The work week had already decreased to 40 hours by 1940.

In contrast, information and communications continued to see dramatic advances:

- Recorded music went from vinyl records to cassette tapes to CDs to MP3s to streaming services

- Recorded video became available, from VHS tapes to DVDs to video streaming

- Televisions got bigger and their pictures became sharper

- Phones went mobile and then turned into pocket computers

- The entire computer and Internet revolution happened

Gordon does not deny the revolution in electronics, computers, and the Internet. The essence of his qualitative argument is this: since 1970, only computing, communications and entertainment have been revolutionized (directly, with some indirect effects on other areas such as retail). But from 1870–1940, everything was transformed: not only communications and entertainment but also food, clothing, the home, transportation, medicine, and work. A revolution in one area of the economy is not, on its own, as big as the combined total of several simultaneous revolutions covering all areas of the economy.

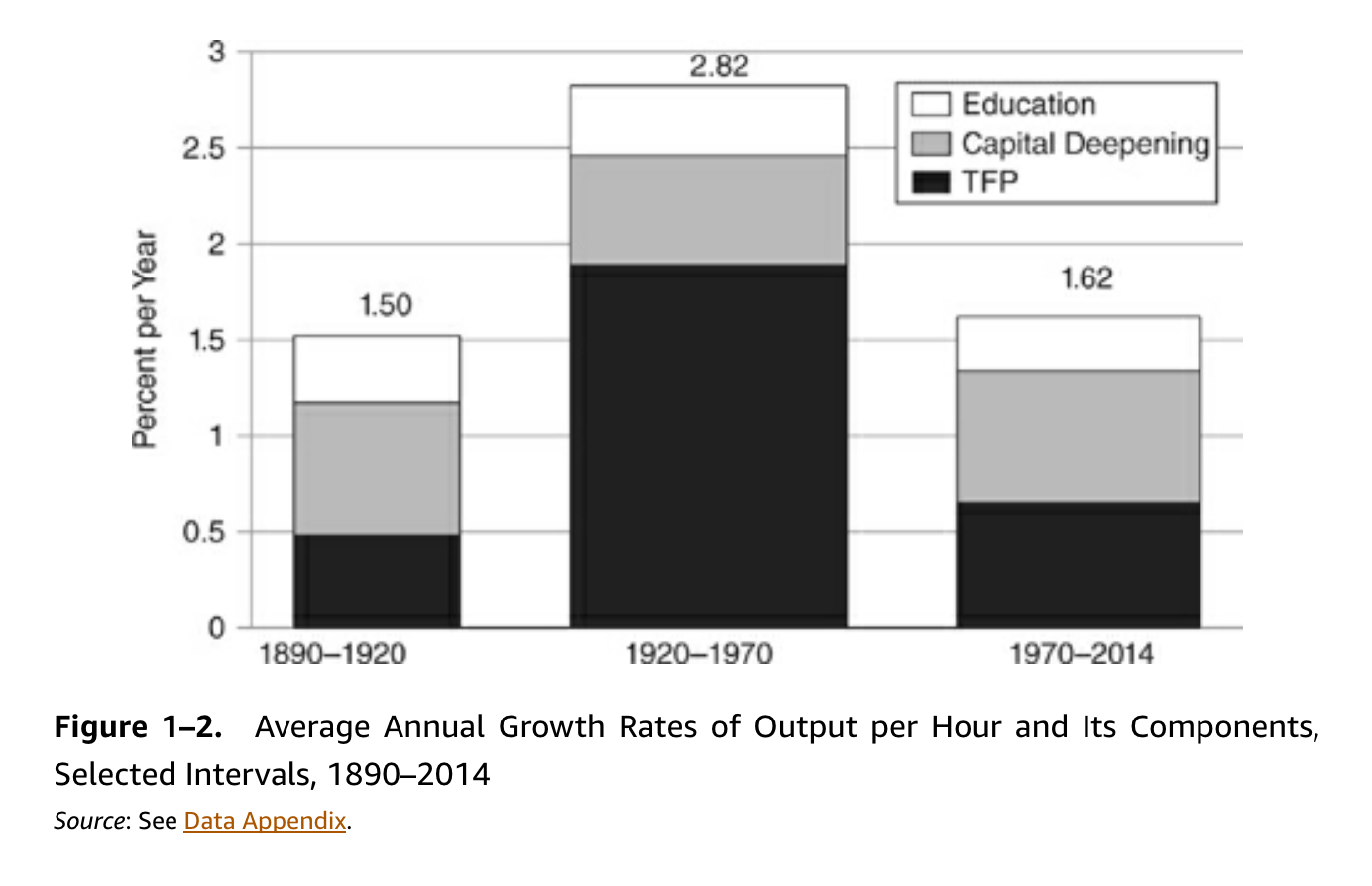

Gordon backs up his qualitative argument with a wealth of data; charts and tables are given throughout the book. A few particularly important ones stand out. One is GDP growth rates, split into three periods:

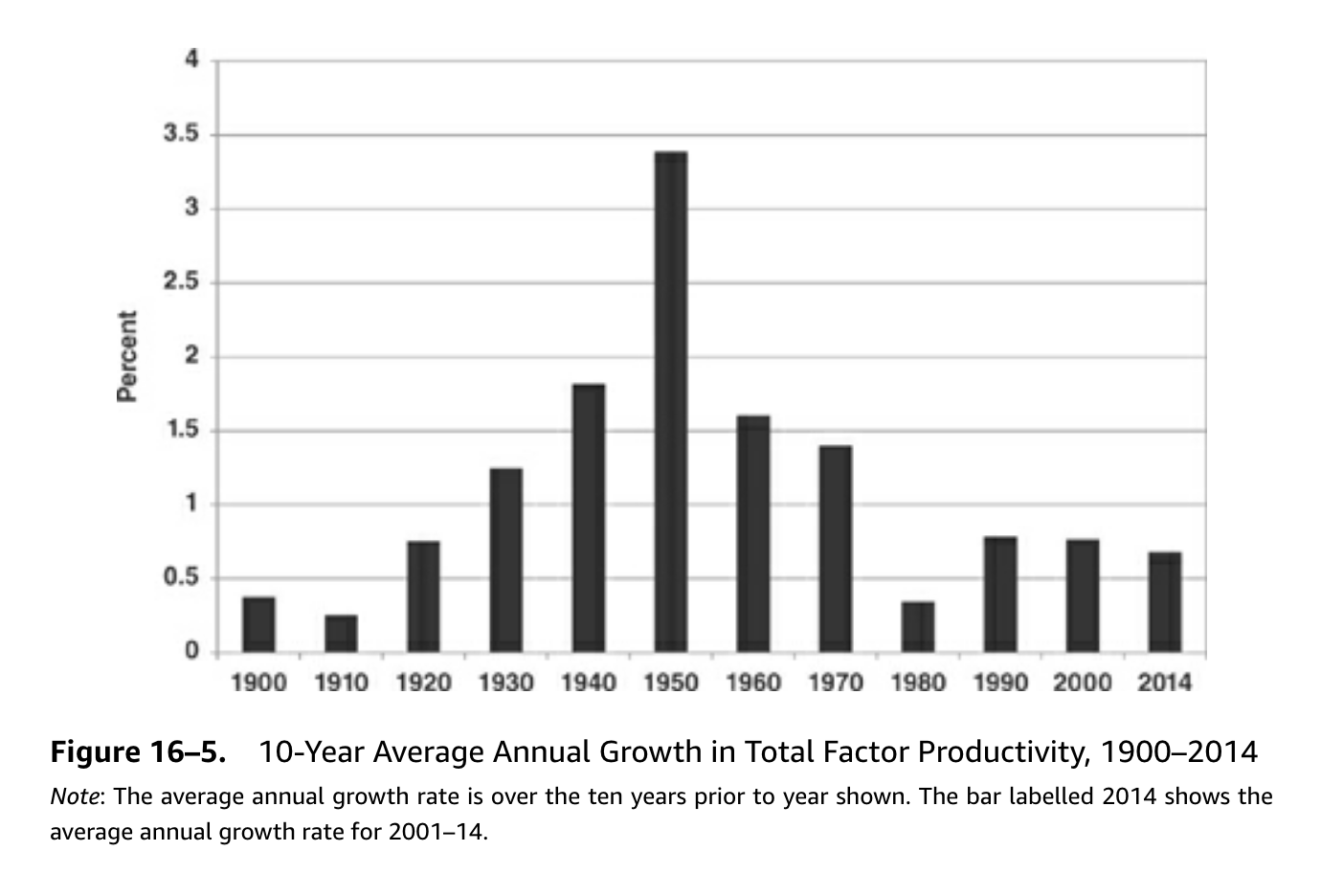

The 1920–70 period stands out as having significantly higher growth than either before or after. Note that increases in capital and labor, including the improved education of the workforce, did not change much across these three periods. Therefore, the difference is mostly from a combination of other factors. Economists refer to this unaccounted-for growth as “total factor productivity” (or TFP), and it is generally assumed to come from advances in technology, organization and management. Gordon shows a breakout of TFP by decade:

If many crucial inventions, such as the sewing machine, electric light and motor, telephone, and automobile, were created in the period 1870–1920, then why was the higher growth not seen until the 1920–70 period? In brief, it took decades for many inventions to be widely distributed and adopted. The electric power industry was created in the 1880s, but electric light didn’t reach 80% penetration until 1940. In that same year, running water was only in 70% of homes, and indoor flush toilets in 60%. The automobile wasn’t widely adopted until Ford brought the price down in the 1910s. Radio was invented prior to 1920, but the radio industry, with networks and programming on the air, didn’t take off until the 1920s. Perhaps most significantly, electricity ultimately led to a revolution in manufacturing, but only after processes and entire factories and were redesigned to take advantage of its possibilities:

The assembly line, together with electric-powered tools, utterly transformed manufacturing. Before 1913, goods were manufactured by craftsmen at individual stations that depended for power on steam engines and leather or rubber belts. The entire product would be crafted by one or two employees. Compare that with a decade later, when each worker had control of electric-powered machine tools and hand tools, with production organized along the Ford assembly-line principle. An additional aspect of the assembly line was that it saved capital, particularly “floor space, inventories in storage rooms, and shortening of time in process.”

It is likely that electric power and the assembly line explain not just the TFP growth upsurge of the 1920s, but also that of the 1930s and 1940s. There are two types of evidence that this equipment capital was becoming more powerful and more electrified. First is the horsepower of prime movers, a data series available for selected years for different types of productive capital, and the second is kilowatt hours of electricity production.

Gordon also traces some of the causes back to the Depression and World War II. The New Deal promoted unionization, which led to rising wages and a shrinking work week, which motivated employers to invest in capital to substitute for labor. During WW2, the urgency and pressure of the threat spurred manufacturers to reach ambitious new levels of efficiency. Two famous examples were the Kaiser shipyards, which in a short period from 1942–43 reduced the time needed to build a Liberty freighter from eight months to a few weeks; and the Ford plant at Willow Run that, before the end of the war, was producing B-24 bomber planes at the rate 432 per month. The federal government helped increase capacity by heavily investing in machine tools, which doubled in number from 1940 to 1945. After the Depression and the war, the new capital equipment, processes, and knowledge didn’t go away, and was turned to the purpose of peacetime production.

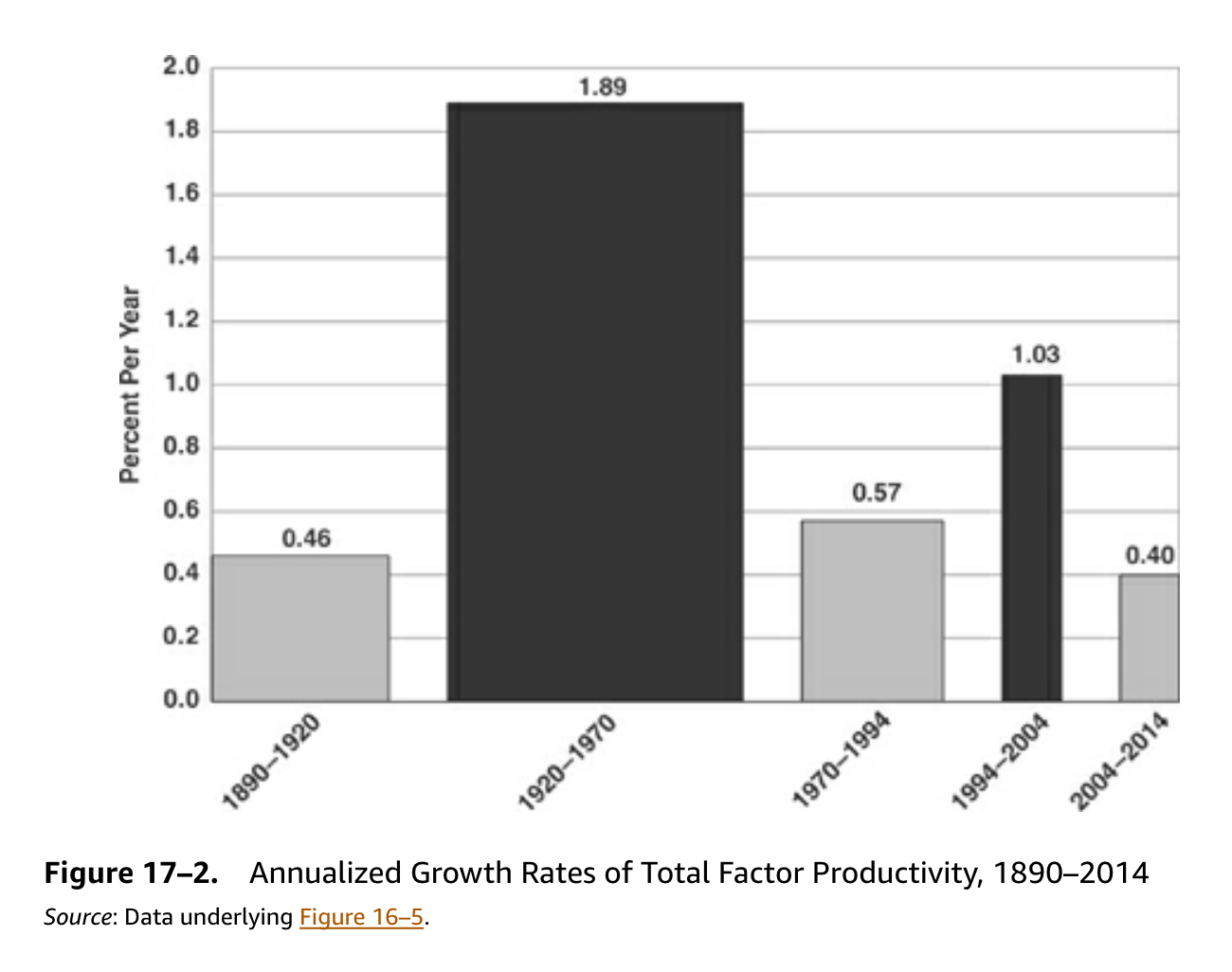

To understand the impact of the digital revolution, Gordon breaks out TFP growth into multiple periods, and isolates in particular the decade 1994–2004:

He ultimately concludes that the digital revolution had a real but comparatively minor impact on the economy: its impact was lower in magnitude and shorter-lived than the combined impact of electricity, the automobile, and the other inventions of the previous period.

A common criticism of this type of analysis is that it relies on GDP, and GDP does not capture all improvements to the quality of life. In the Internet era, many of the best services, such as Google, Wikipedia, and YouTube, are free—an enormous consumer surplus that doesn’t contribute to GDP. Gordon agrees with this point, but he argues that this has always been the case, and that in fact even more consumer surplus went unmeasured in the past, such as the value of free radio and television programs, the liberation provided by the automobile, or the lives saved by penicillin. Thus, he argues, GDP mismeasurement can’t explain the GDP growth slowdown.

What about the future? Gordon is not optimistic.

The trends of the early and mid-20th century are mostly played out. Our factories are already electrified, as are our homes. Everyone already has a car, a phone, and a toilet.

Even computing, Gordon thinks, has mostly given us its contribution already, citing the slowing of TFP growth after 2004. Business practices haven’t changed much since we all got PCs, spreadsheets, and email. Retail hasn’t changed much since computerized inventories and barcode scanners. Banking has already deployed ATMs, and the financial markets are already computerized. The smartphone has matured and plateaued, and after it, there isn’t much that’s new in consumer electronics. Even Moore’s Law is slowing down.

The demographic changes of the 20th century that improved productivity also don’t have much further to go. The share of the population living in urban areas hit 70% by 1960. High school graduation rates rose from 9% in 1910 to 77% by 1970, but aren’t much higher today. The labor force participation rate of women rose dramatically after the war but peaked at 77% in 1999, and is now a bit lower.

What about new technologies? Gordon has surveyed the field and is unimpressed. Drug development is just getting more expensive. Robots aren’t good enough to replace humans yet. 3D printing won’t replace mass production. “Big data” is just a continuation of the trend towards more data and therefore is nothing new. Self-driving cars won’t shorten people’s commutes, and self-driving trucks won’t replace all the functions of drivers, who also load and unload the trucks and stock store shelves. And besides, self-driving vehicles don’t work yet anyway.

Finally, Gordon sees “headwinds” working against growth. The boomers are retiring. Debt is rising, including student debt (now over $1 trillion) and government debt (which is nearing 100% of GDP). And inequality is growing, so gains in GDP per capita will translate to smaller gains in median income.

Taking all factors into account, Gordon forecasts an average growth rate of just 0.3% in real median disposable income per person over the period 2015–2040, compared to 2.25% growth 1920–70 and 1.46% 1970–2014.

Can we do anything about it?

In a postscript, Gordon offers a long list of policy prescriptions, including:

- Higher taxes on the very rich

- Increase in the minimum wage

- Expanded Earned Income Tax Credit

- Mass pardoning to reduce the incarceration rate

- Drug legalization

- Public preschool

- Financing public school with statewide rather than local sources to reduce school inequality

- Publicly funded college, paid for by higher income taxes on college graduates

- Restrictions on patents and copyrights

- Reduced occupational licensing

- Reduced zoning and land-use regulations

- More high-skill immigration

- Eliminating tax deductions

- A carbon tax

These prescriptions, however, are only palliative. Fundamentally, he sees the growth slowdown as so natural and inevitable that it is not even to be lamented:

What is remarkable about the American experience is not that growth is slowing down but that it was so rapid for so long…. the rise and fall of growth are inevitable when we recognize that progress occurs more rapidly in some time intervals than in others. There was virtually no economic growth for millennia…. American growth slowed down after 1970 not because inventors had lost their spark or were devoid of new ideas, but because the basic elements of a modern standard of living had by then already been achieved along so many dimensions, including food, clothing, housing, transportation, entertainment, communication, health, and working conditions.

The 1870–1970 century was unique: Many of these inventions could only happen once, and others reached natural limits.

There is no murder investigation, because there was no murder. The victim died of natural causes.

I found the first two parts of the book very valuable. The survey of improvements to the American standard of living over the last 150 years is comprehensive, described in vivid detail, and quantified with more than enough charts and tables. As an overview of progress, it is excellent. If the phrase “standard of living” (which I have always found vapid) is an empty term to you, this book will fill it with many colorful examples.

But I find Gordon’s vision for the future strangely lacking in imagination, and his complacent acceptance of low growth disappointing. Contrast this with another proponent of the stagnation hypothesis, Peter Thiel. Thiel’s view seems to be not that stagnation was natural or inevitable, but that we dropped the ball, and that we should have had flying cars by now.

In considering potential future technological developments in one of the final chapters, Gordon only considers four: “medical, small robots and 3D printing, big data, and driverless vehicles.” And he doesn’t actually analyze the future of these technologies, but instead looks only at their present. He points out that at one robot competition, the robots had trouble standing up; that robotic reasoning is limited, and that they can enter an error state if presented with an unfamiliar situation; that self-driving cars only work at low speeds and depend on detailed maps. Given that this comes after several hundred pages detailing over a century of breakthrough inventions, there is surprisingly little recognition that technologies almost always go through an immature stage in which they do not work reliably, and that eventually these problems are solved through engineering iteration. Gordon also shows little imagination for the economic potential of self-driving vehicles, assuming that we will continue to use cars and trucks in the same way, only without drivers. He does not seem to consider that self-driving vehicles have the potential to fundamentally alter land use patterns and cargo logistics, even though he described in earlier chapters how motor vehicles did exactly these things.

There is no serious consideration that we might solve other grand challenge problems, such as curing cancer or heart disease the way we cured infectious diseases and vitamin deficiencies, or generating cheap and safe nuclear power. The possibility that we might make new breakthroughs in areas such as genetic engineering or quantum computers is not raised.

I find this approach difficult to understand. It seems to treat centuries of breakthroughs as … a fluke.

That said, I think this is overall a very valuable book that every serious student of progress should read. It is an excellent survey of American growth, and it paints the stagnation picture clearly.

And even its predictions for the future are valuable if taken, not as a prophecy, but as a warning. A 0.3% growth rate is the future—if we have no more breakthroughs. We have, in some ways, been coasting on the achievements of the past. Gordon shows us that all inventions, no matter how great, eventually mature and plateau. Restoring high growth will require new fundamental inventions and possibly entire new fields of science. I’m becoming increasingly convinced that this is where progress studies should focus.

Relevant books

The Rise and Fall of American Growth